One of the biggest challenges for FRM aspirants is understanding the syllabus and exam structure. Many students feel overwhelmed because they are not sure what to study, how deep to go, and what the exam actually tests.

In reality, once you understand the structure clearly, FRM becomes much more manageable.

In this guide, we will break down the FRM syllabus and exam pattern for both Level 1 and Level 2 with practical clarity.

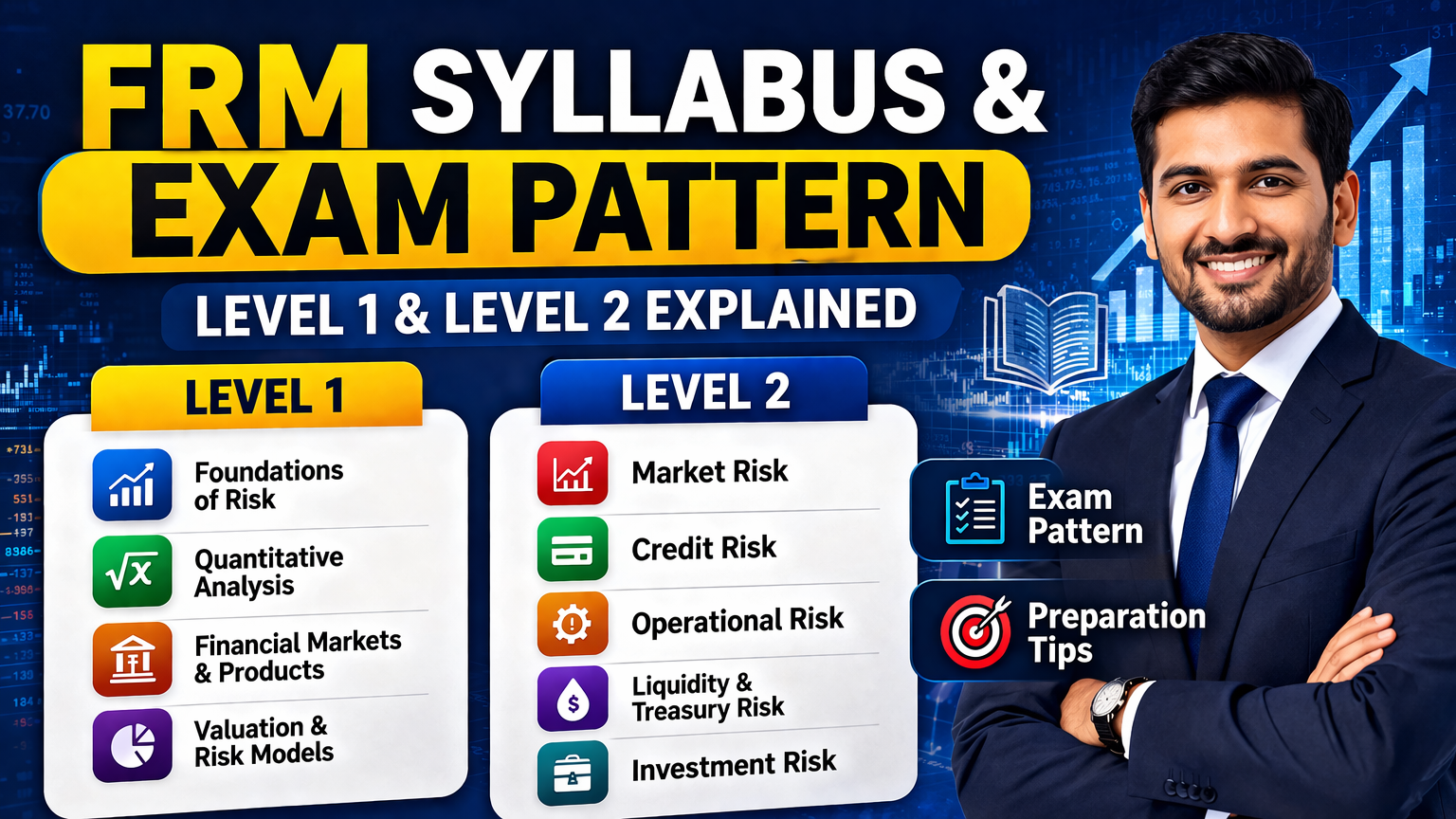

Overview of FRM Exam Structure

FRM is divided into two levels

Level 1 focuses on concepts and fundamentals

Level 2 focuses on application and real world scenarios

Both levels must be cleared to complete the FRM program.

FRM Level 1 Syllabus

Level 1 builds your foundation in risk management. It focuses on understanding tools, concepts, and financial markets.

1 Foundations of Risk Management

This section introduces the core concepts of risk.

You learn

Types of financial risks

Role of risk management in organizations

Basel regulations basics

Example

Understanding how banks measure and manage risk exposure in lending.

2 Quantitative Analysis

This is one of the most important sections.

You learn

Probability concepts

Statistical measures

Regression analysis

Time value of money

Example

Calculating probability of default or expected loss using statistical models.

3 Financial Markets and Products

This section helps you understand how financial instruments work.

You learn

Bonds

Derivatives

Options and futures

Interest rates

Example

Understanding how bond prices change with interest rates.

4 Valuation and Risk Models

This section connects theory with application.

You learn

Value at Risk

Risk measurement models

Portfolio risk

Example

Estimating how much money a portfolio could lose under worst case scenarios.

Level 1 Weightage (Approx)

Foundations of risk management

Quantitative analysis

Financial markets

Valuation models

Quantitative and valuation topics usually carry significant weight.

FRM Level 2 Syllabus

Level 2 is more practical and focuses on real world application of risk concepts.

1 Market Risk Measurement and Management

You learn

Interest rate risk

Equity risk

Currency risk

Stress testing

Example

Analyzing how a portfolio reacts to market crashes.

2 Credit Risk Measurement and Management

This is highly relevant for banking roles.

You learn

Credit rating models

Default risk

Credit derivatives

Example

Evaluating whether a company is likely to default on its loan.

3 Operational Risk and Resilience

You learn

Business risks

Fraud risk

System failures

Risk mitigation strategies

Example

Managing risks related to internal processes or cyber threats.

4 Liquidity and Treasury Risk

You learn

Liquidity management

Funding risk

Cash flow management

Example

Ensuring a bank has enough cash to meet withdrawal demands.

5 Risk Management and Investment Management

This section connects risk with investment decisions.

You learn

Portfolio risk

Asset management

Hedging strategies

Level 2 Weightage (Approx)

Market risk

Credit risk

Operational risk

Liquidity risk

Investment risk

Level 2 focuses more on practical scenarios and case based understanding.

FRM Exam Pattern

Understanding the pattern is equally important.

Level 1 Exam Pattern

100 multiple choice questions

Duration around 4 hours

Focus on concepts and calculations

Level 2 Exam Pattern

80 multiple choice questions

Duration around 4 hours

Focus on application and interpretation

Difficulty Level of FRM Exams

FRM is considered challenging because

Questions test concepts deeply

Application based thinking is required

Time management is important

Example

Instead of asking definitions, the exam may present a scenario and ask you to apply a concept.

How to Approach the Syllabus

Many students make the mistake of studying randomly.

Here is a smarter approach.

Step 1 Start with Foundations

Build strong basics before moving to advanced topics.

Step 2 Focus on Quantitative Concepts

Quantitative analysis is the backbone of FRM.

Spend extra time here.

Step 3 Practice Questions Regularly

FRM is application based.

Solving questions is more important than just reading theory.

Step 4 Revise Multiple Times

Concepts require revision to become clear.

Real Life Study Strategy Example

Let us take an example.

A student studies for 4 months.

Month 1

Foundations and basic concepts

Month 2

Quantitative analysis

Month 3

Markets and valuation

Month 4

Revision and mock tests

This structured approach improves chances of success.

Common Mistakes Students Make

Ignoring quantitative topics

Focusing only on theory

Not practicing enough questions

Skipping revision

Avoiding these mistakes can significantly improve performance.

Final Thoughts

The FRM syllabus is comprehensive but highly practical. It is designed to prepare candidates for real world risk management roles.

Level 1 builds your foundation, while Level 2 develops your ability to apply concepts in real scenarios.

Once you understand the structure and follow a disciplined study plan, FRM becomes much more manageable.

The key is consistency, practice, and clarity of concepts.