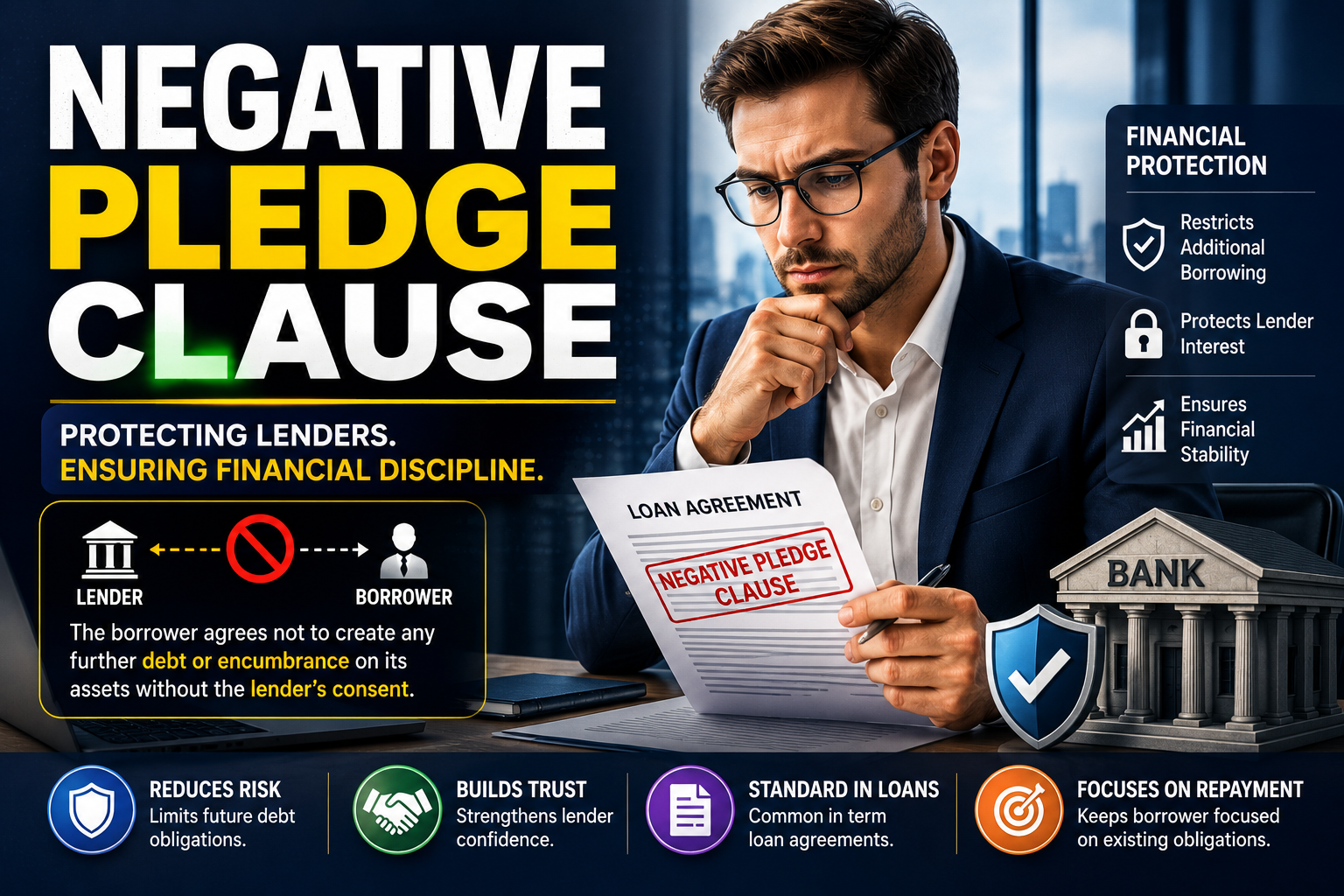

A negative pledge clause is a condition in a loan or bond agreement that stops the borrower from giving better security to another lender without protecting the existing lender.

It is mostly used in debt contracts.

The idea is simple. If a lender gives money to a company without strong collateral, the lender does not want the company to later give all its valuable assets as security to someone else. That would make the first lender weaker.

So, the negative pledge clause protects lenders from being pushed behind other creditors.

What is a Negative Pledge Clause?

A negative pledge clause restricts the borrower from creating new secured debt over its assets unless the existing lender is treated equally.

In simple words, the borrower cannot say:

“I will give my best assets as security to a new lender, but the old lender will remain unsecured.”

The clause does not always stop the borrower from taking new loans. It mainly controls whether the borrower can use its assets as security for another lender.

This helps maintain fairness among lenders.

Simple Example

Suppose ABC Ltd borrows ₹100 crore from Bank A.

Bank A gives the loan without taking any specific property or machinery as collateral.

Later, ABC Ltd wants to borrow another ₹50 crore from Bank B.

Bank B asks ABC Ltd to give its factory land as security.

Now, if ABC Ltd gives the factory land only to Bank B, Bank B becomes a secured lender. Bank A remains unsecured.

This creates a problem for Bank A.

If ABC Ltd faces financial trouble later, Bank B will have first claim over the factory land. Bank A may recover much less.

To avoid this, Bank A may include a negative pledge clause in the original loan agreement.

This clause says that ABC Ltd cannot create security over its assets for another lender unless Bank A also gets similar protection.

Real Life Context

Think of a company that raises money through unsecured bonds.

Bond investors agree to invest because the company has strong assets and a good credit profile.

But after issuing the bonds, the company takes a new bank loan and gives its major assets as collateral.

Now the bank becomes secured, while bondholders remain unsecured.

If the company defaults, the secured bank loan will have better recovery rights. The bondholders may be left with weaker protection.

This is exactly the situation a negative pledge clause tries to prevent.

It gives comfort to existing lenders that the borrower will not reduce their position by pledging key assets elsewhere.

Why Lenders Use It

Lenders use negative pledge clauses to protect their credit position.

The clause helps ensure that the borrower does not increase secured borrowing in a way that harms existing lenders.

It is especially important when the original loan or bond is unsecured.

Without this clause, a borrower could take more loans and pledge valuable assets to new lenders, reducing the recovery chances for old lenders.

Why Borrowers Agree to It

Borrowers agree to a negative pledge clause because it may help them raise debt at better terms.

If lenders feel protected, they may accept a lower interest rate or provide a larger loan amount.

However, the borrower gives up some flexibility.

After signing such a clause, the borrower cannot freely use its assets as collateral for future borrowing.

So, it is a trade-off between lower borrowing cost and financial flexibility.

Negative Pledge vs Collateral

A negative pledge is not the same as collateral.

Collateral gives a lender a direct claim over a specific asset.

A negative pledge does not create direct security.

It only restricts the borrower from giving security to others without also protecting the existing lender.

So, collateral is an asset-based protection.

A negative pledge is a contractual protection.

Key Risk for Lenders

A negative pledge clause is useful, but it is not as strong as actual collateral.

If the borrower violates the clause, the lender may have legal rights under the contract. But the lender may still not have a direct claim over the pledged asset unless the agreement provides for it.

That is why lenders still need to study the borrowers credit quality, debt level, asset base, and other loan covenants.

Final Thoughts

A negative pledge clause is a protective condition in a loan or bond agreement.

It stops the borrower from giving security to new lenders in a way that weakens existing lenders.

The simple way to remember it is this:

A negative pledge clause says that the borrower cannot pledge important assets to another lender without giving similar protection to the existing lender.