Whenever money is lent, there is always a possibility that it may not be repaid. This uncertainty is known as credit risk.

Credit risk is one of the most important concepts in finance and forms the backbone of banking and lending systems. Whether it is a bank giving loans, an investor buying bonds, or a company extending credit to customers, credit risk is always present.

In this guide, we will break down credit risk in a simple and practical way with real life examples, types, and insights.

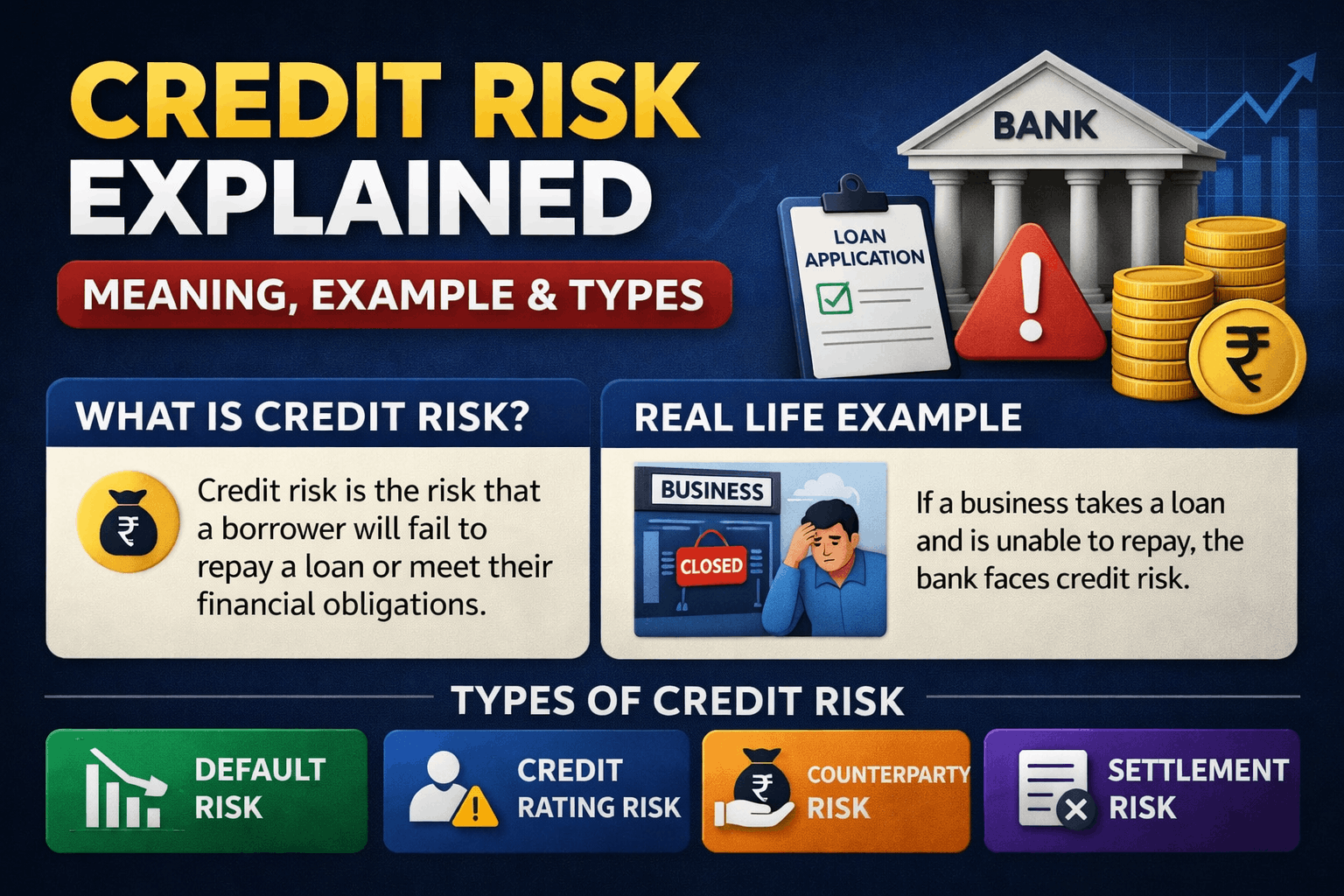

What is Credit Risk

Credit risk is the risk that a borrower fails to repay a loan or meet their financial obligations.

👉 In simple terms

Credit risk is the risk of losing money because someone does not pay back what they owe

Why Credit Risk is Important

Credit risk is crucial because it directly impacts

Banks and financial institutions

Investors in bonds

Businesses offering credit

Overall financial stability

Example

If banks give loans without properly assessing credit risk, they may face large losses due to defaults. This can lead to financial crises.

Real Life Example of Credit Risk

Let us understand this with a simple example.

A bank gives a loan of 10 lakh to a small business.

Due to poor business performance, the company is unable to repay the loan.

The bank loses a significant portion of the money.

👉 This loss is caused by credit risk

Where Credit Risk Exists

Credit risk is present in many financial activities.

Bank loans

Corporate bonds

Credit cards

Trade credit between businesses

Even when you use a credit card, the bank is exposed to credit risk.

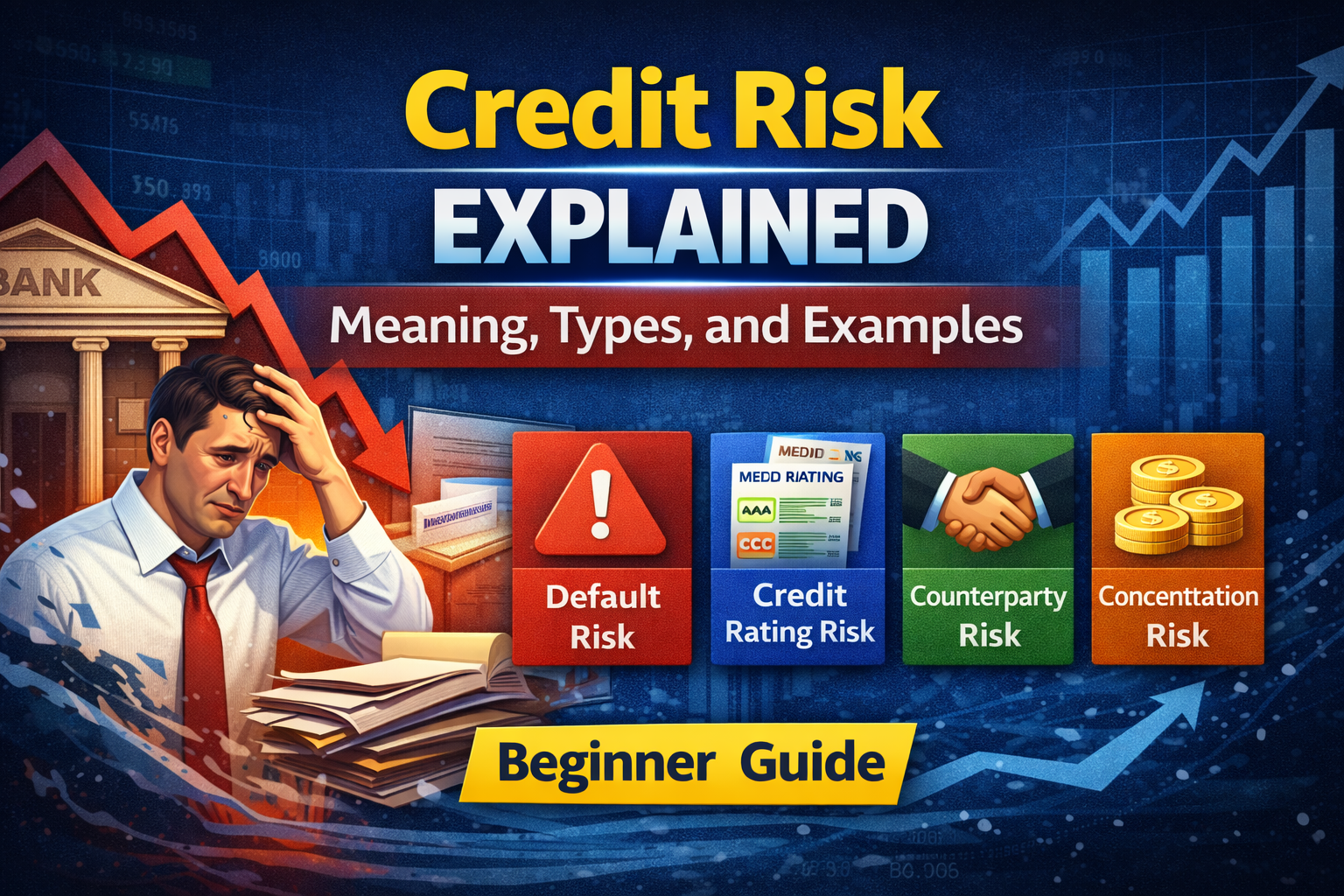

Types of Credit Risk

Credit risk is not just about default. It includes multiple forms of risk.

1 Default Risk

Default risk is the most basic type of credit risk.

It occurs when a borrower completely fails to repay the loan.

Example

A borrower stops paying loan installments due to financial difficulties.

2 Credit Rating Risk

This risk arises when the creditworthiness of a borrower deteriorates.

Even if the borrower does not default, their financial condition weakens.

Example

A company’s credit rating is downgraded from AAA to BBB.

This increases risk and reduces the value of its bonds.

3 Counterparty Risk

This occurs in financial transactions where one party may fail to fulfill its obligation.

It is common in derivatives and financial contracts.

Example

In a derivative contract, one party fails to make the required payment.

4 Concentration Risk

This occurs when too much exposure is given to a single borrower or sector.

Example

A bank lends a large portion of its funds to one industry.

If that industry faces a downturn, the bank faces significant losses.

Causes of Credit Risk

Credit risk arises due to multiple factors.

1 Poor Financial Health of Borrower

If the borrower has weak financials, repayment becomes uncertain.

2 Economic Conditions

During economic downturns, businesses struggle and defaults increase.

3 Lack of Proper Risk Assessment

If lenders do not evaluate borrowers properly, risk increases.

4 Over Lending

Giving too much credit without proper checks increases exposure.

How Banks Assess Credit Risk

Banks use various methods to evaluate credit risk before giving loans.

1 Credit Score

Individuals are evaluated using credit scores.

Higher score means lower risk.

2 Financial Statement Analysis

Companies are assessed based on

Revenue

Profitability

Debt levels

3 Collateral

Banks often require assets as security.

Example

Home loans are secured by property.

4 Credit Rating Agencies

Agencies like Moody’s and S&P rate companies based on risk.

How to Manage Credit Risk

Credit risk cannot be eliminated but can be managed effectively.

1 Diversification

Lending to multiple borrowers reduces overall risk.

2 Credit Analysis

Proper evaluation before lending reduces default probability.

3 Collateral Requirement

Securing loans with assets reduces potential losses.

4 Monitoring Borrowers

Regularly tracking borrower performance helps detect early warning signs.

Credit Risk vs Market Risk

Many beginners confuse these two.

Credit Risk

Loss due to borrower default

Market Risk

Loss due to market fluctuations

Example

Loan not repaid → Credit risk

Stock price falls → Market risk

Real Life Scenario

Consider two banks.

Bank A gives loans without proper checks and faces high defaults.

Bank B carefully evaluates borrowers and diversifies its loans.

Bank B performs better because it manages credit risk effectively.

Importance of Credit Risk in FRM

Credit risk is a core subject in FRM certification.

FRM teaches

How to measure credit risk

How to model default probability

How to manage exposure

Career roles include

Credit analyst

Risk analyst

Banking professional

Common Mistakes Beginners Make

Assuming all borrowers will repay

Ignoring credit ratings

Overexposure to one borrower

Not understanding risk properly

Final Thoughts

Credit risk is one of the most fundamental risks in finance. It directly affects banks, investors, and businesses.

Understanding credit risk helps in making better financial decisions, whether you are lending money, investing in bonds, or working in finance.

The key is not to avoid risk completely but to assess and manage it intelligently.

If you are preparing for FRM or building a career in finance, mastering credit risk is essential.