Risk is an unavoidable part of finance. Every decision, whether it is lending money, investing in markets, or running a business, involves uncertainty.

However, successful financial institutions are not those that avoid risk, but those that manage risk effectively.

This is where the risk management process becomes critical.

In this guide, we will break down how banks and financial institutions identify, measure, control, and monitor risks in a structured way.

What is Risk Management

Risk management is the process of identifying, assessing, and controlling financial risks to minimize losses.

👉 In simple terms

Risk management is about understanding what can go wrong and taking steps to reduce its impact

Why Risk Management is Important

Risk management is essential because it helps

Protect financial institutions from losses

Ensure business stability

Maintain investor confidence

Comply with regulations

Example

If a bank does not manage risks properly, it may face large losses due to loan defaults, market crashes, or operational failures.

Types of Risks Managed

Financial institutions manage multiple types of risks.

Market risk

Credit risk

Liquidity risk

Operational risk

These risks are interconnected and require a structured approach.

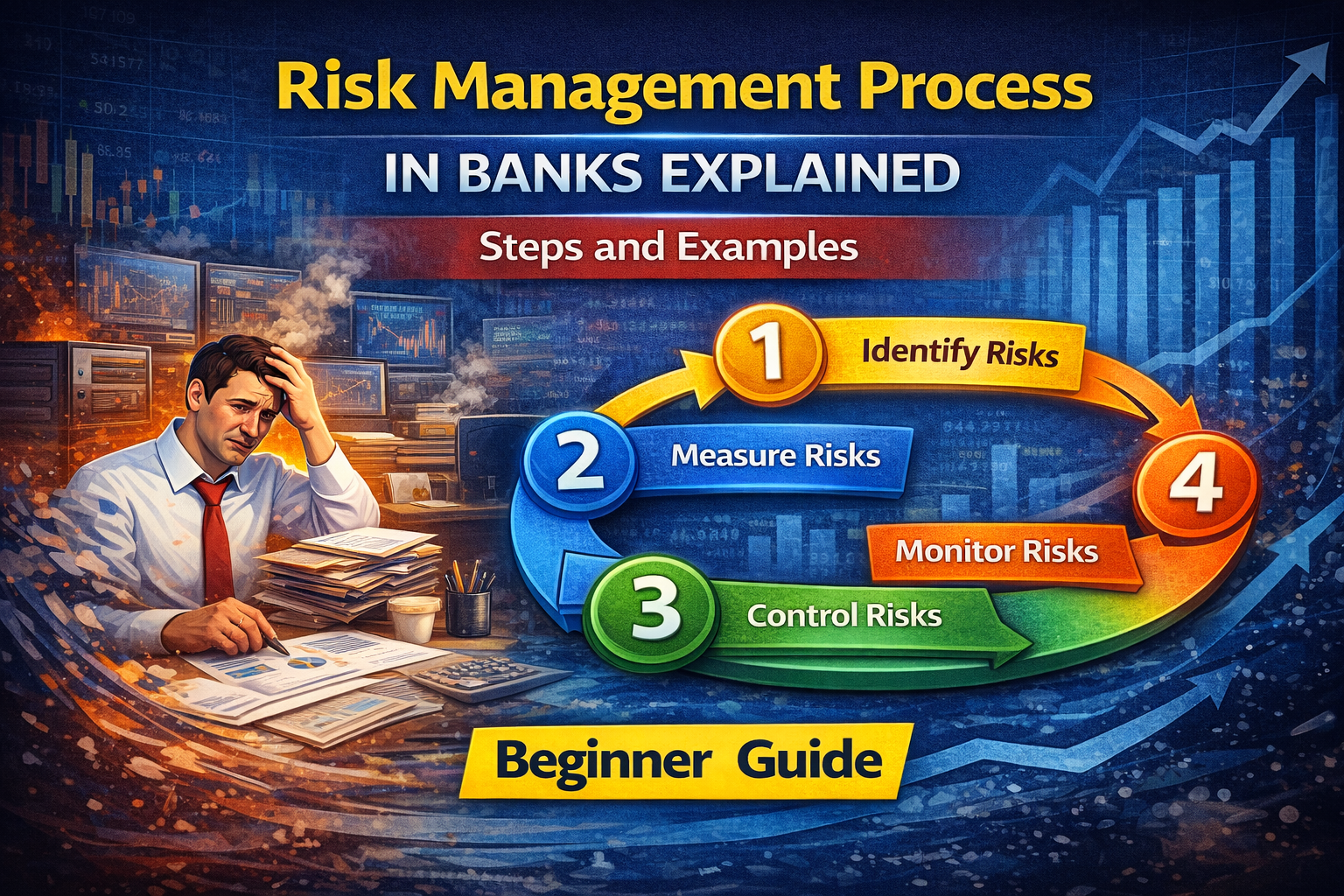

The Risk Management Process

The risk management process follows a systematic approach.

Step 1 Risk Identification

The first step is identifying potential risks.

This involves understanding what could go wrong.

Example

A bank identifies risks such as

Loan defaults

Interest rate changes

System failures

Key Insight

If risks are not identified early, they cannot be managed effectively.

Step 2 Risk Measurement

Once risks are identified, the next step is measuring them.

This helps in understanding the potential impact.

Tools Used

Value at Risk

Stress testing

Scenario analysis

Example

A bank estimates how much loss it could face if interest rates rise by 2 percent.

Key Insight

Measuring risk helps institutions prepare for worst case scenarios.

Step 3 Risk Control and Mitigation

After measuring risks, institutions take steps to reduce or control them.

Common Strategies

Diversification

Hedging

Setting exposure limits

Using collateral

Example

A bank limits the amount it lends to a single borrower to reduce concentration risk.

Key Insight

Risk cannot be eliminated, but it can be controlled.

Step 4 Risk Monitoring

Risk management is not a one time activity. Risks must be continuously monitored.

Example

Banks track

Loan performance

Market movements

Liquidity levels

Key Insight

Continuous monitoring helps detect problems early.

Step 5 Risk Reporting

Financial institutions regularly report risks to management and regulators.

Example

Risk reports include

Exposure levels

Loss estimates

Risk trends

Key Insight

Transparency is essential for effective risk management.

Real Life Example of Risk Management

Let us understand with a simple scenario.

A bank notices an increase in loan defaults.

Step 1

It identifies rising credit risk

Step 2

Measures potential losses

Step 3

Tightens lending rules

Step 4

Monitors loan performance

Step 5

Reports risk to management

This structured process helps the bank reduce losses.

Tools Used in Risk Management

Financial institutions use advanced tools.

Value at Risk (VaR)

Estimates potential loss under normal conditions

Stress Testing

Tests performance under extreme conditions

Scenario Analysis

Analyzes impact of different scenarios

Risk Management in Banks vs Companies

Banks

Focus heavily on

Credit risk

Liquidity risk

Market risk

Companies

Focus on

Operational risk

Market exposure

Cash flow management

Common Mistakes in Risk Management

Ignoring early warning signs

Overexposure to single risk

Lack of diversification

Weak monitoring systems

Importance of Risk Management in FRM

Risk management is the core of FRM certification.

FRM focuses on

Risk identification

Risk measurement

Risk control techniques

Career Roles

Risk analyst

Risk manager

Compliance officer

Treasury professional

Real Life Scenario

Consider two banks.

Bank A has a strong risk management system.

Bank B ignores risk controls.

During a financial crisis, Bank A survives while Bank B faces heavy losses.

The difference is effective risk management.

Future of Risk Management

With advancements in technology, risk management is evolving.

Use of data analytics

Artificial intelligence

Real time risk monitoring

These tools help institutions manage risks more efficiently.

Final Thoughts

Risk is an unavoidable part of finance, but it can be managed effectively with the right approach.

The risk management process provides a structured way to identify, measure, and control risks.

Whether you are an investor, a finance professional, or preparing for FRM, understanding risk management is essential.

The goal is not to eliminate risk but to manage it intelligently and strategically.